JUST THE FACTS

SUMMARIZED AND EVIDENCE SUPPORTED

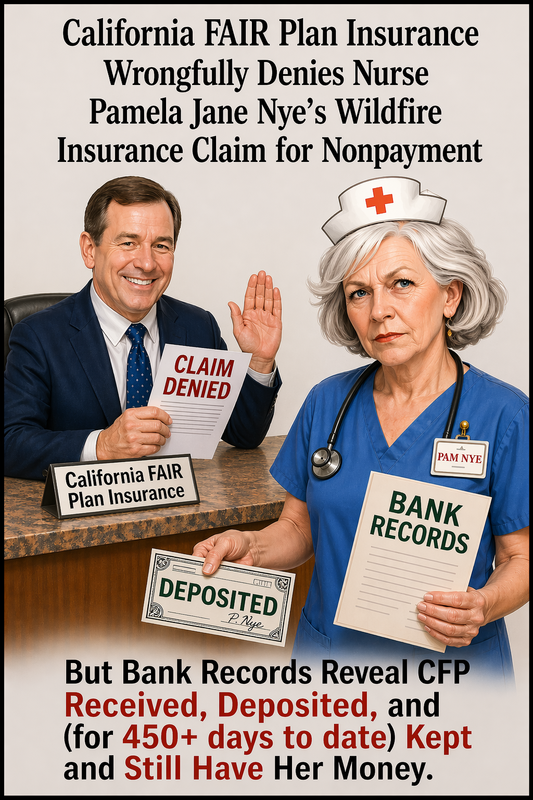

- Bank records confirm that on November 1, 2024 California Fair Plan (CFP) received and subsequently deposited nurse Pamela Jane Nye's annual insurance policy renewal check dated October 23, 2024 and for the correct amount of $2,943.

- CFP failed to provide any evidence proving Nye accepted, deposited or cashed their California FAIR Plan refund.

- CFP admits that since January 1, 2024, it kept, and continues to keep Nye's $2.934 insurance policy renewal payment funds.

- 09/22/2025 and 09/23/2025 CFP records confirm payment receipt and denial of Nye's insurance claim.

- 11/06/2025 CFP's CEO and claims department received copies of Nye's claim appeal and supportive documents.

- CFP Claims staff told Nye to speak with her Farmers insurance agents because they were "sent copies of payment due, late payment warnings, cancellation and premium return notices."

- March 10, 2026: Nye files a help Complaint with California Insurance Commission which is currently being investigated.

- July **, 2026: Nye's attorney files ##-page lawsuit in California Superior Court/Los Angeles (Case No: ***********) naming Defendant parties California FAIR Plan, Farmers Insurnace Group, Farmers Insurace Exchange and Nye's Farmers Insurance Agents Michael Rey and Patrick Prendiville.

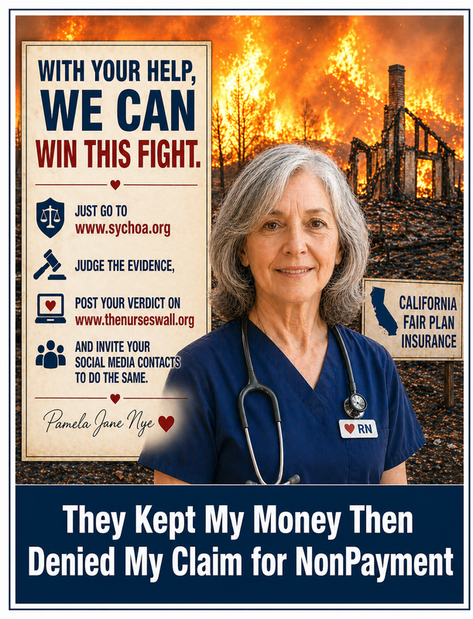

"Let’s put ‘FAIR’ back into Pamela Jane Nye's FAIR Plan insurance claim!"

EXHIBIT LINKS BELOW ARE HTTPS CERTIICATE PROTECTED:

- EXHIBIT 00 2024-2025 CFP Policy Renewal Docs Un known by Nye until claim filed)

- EXHIBIT 01 Initial Appeal to CFP Claims Dept and Denial Response

- EXHIBIT 02 Appeal Letter to CFP/CEO Victoria Roach

- EXHIBIT 03 Bank Records of Nyes CFP Policy Payment to, and deposit by CFP

- EXHIBIT 04 CFP Denies Nye's Claim Appeal

- EXHIBIT 05A By Certified Mail, CFP sent Nye-requested documents to her wildfire-destroyed address

- EXHIBIT 05B Certified Mail tracking report reveals 15-day delivery

- EXHIBIT 06 2nd appeal for Exec Mgmt.review request directed by CFP

- EXHIBIT 07 CFP Billing Dept responds to McLean-directed Exec. Mgmt.

appeal review and again denies Nye's claim?

- EXHIBIT 08 Nye's CFP claim-related wildfire website pages

- EXHIBIT 09 3/10/2026 Nye' files help request from Calif Dept. of Ins.

- EXHIBIT 10 Retransmitted Appeal for Exec Level review

[Links in Exhibit #11 duplicate what's on this page and are disabled)

- EXHIBIT 12 3/29/2026: FedEx envelope with "DC Fire Return Refund"

check was left on H/Bch residence porch

- EXHIBIT 13 5/14/2026: CFP's Executive Level Appeal Denial.

NEXT: